- VantageScore Uses Large Alternative Data Sets to Pinpoint Creditworthy Mortgage Borrowers Forgotten by Obsolete Models, Including FICO 10T

- New VantageScore 4.0 Mortgage Lending Opportunities Extend Far Beyond First-Time Homebuyers

- New VantageScore 4.0 Qualifying Mortgages Demonstrate Similar or Lower Risk Compared to Historical Mortgage Loans

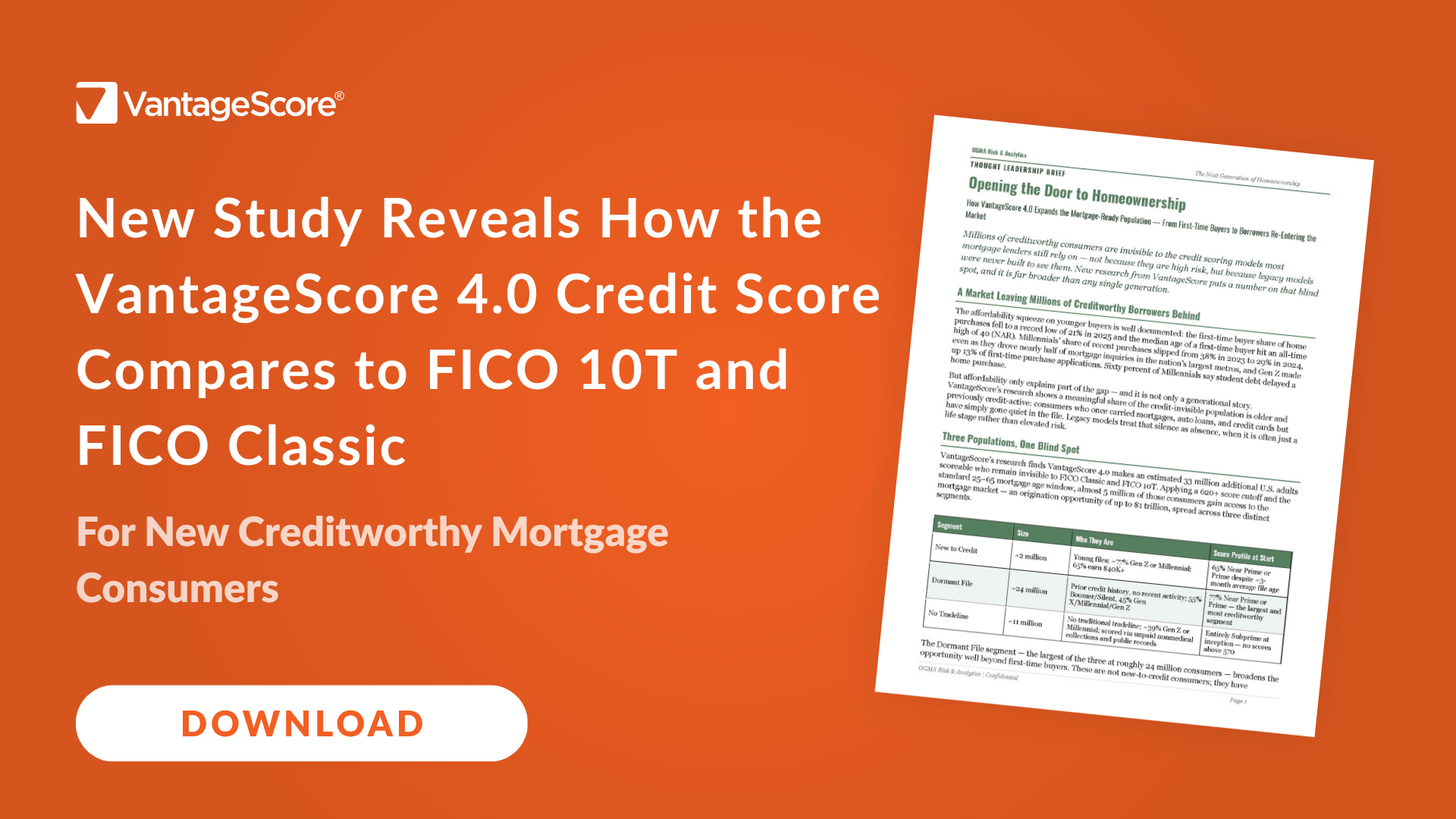

SAN FRANCISCO--(BUSINESS WIRE)--New independent research reveals that nearly five million additional U.S. consumers become mortgage eligible when evaluated using VantageScore 4.0, representing an estimated $1 trillion lending opportunity for mortgage lenders without lowering underwriting standards. The research study issued today by OGMA Risk & Analytics1, titled Opening the Door to Homeownership: How VantageScore 4.0 Expands the Mortgage-Ready Population—From First-Time Buyers to Borrowers Re-Entering the Market, demonstrates that VantageScore 4.0 responsibly expands the mortgage market by identifying more qualified borrowers. VantageScore 4.0 is currently the only FHFA-approved mortgage credit score that scores this expanded population, making it the only model whose full market-expansion value even shows up in an evaluation designed to test for it. In a housing market where affordability, access, and borrower growth are critical, the ability to identify new mortgage consumers is a significant competitive advantage, and only VantageScore 4.0 offers it.

"Our research shows that millions of creditworthy consumers are hiding in plain sight because credit scoring models like FICO Classic and FICO 10T simply weren't designed to recognize them," said Matt Komos, OGMA Risk & Analytics. "The opportunity extends far beyond first-time homebuyers to include experienced, creditworthy borrowers whose credit report histories may have become more aged. By leveraging modern credit analytics and alternative data, lenders can responsibly expand access to homeownership while maintaining the same rigorous approach to credit risk."

The research found that VantageScore 4.0 makes approximately 33 million more U.S. adults scoreable than FICO Classic or FICO 10T. Applying a 620+ mortgage score threshold identifies nearly 5 million additional mortgage-ready consumers spanning three distinct borrower populations: new-to-credit consumers, borrowers with dormant credit files, and consumers with no traditional tradelines.

Further, the largest newly scoreable segment consists of approximately 24 million dormant-file consumers—borrowers with established credit histories whose files have become inactive over time. Despite their lack of recent credit activity, 77% score Near Prime or Prime using VantageScore 4.0, highlighting an overlooked population of experienced borrowers who may be ready to re-enter the mortgage market.

Key insights from the study include:

LARGE ALTERNATIVE DATA SETS HELP REVEAL CREDITWORTHY BORROWERS FORGOTTEN BY OBSOLETE MODELS LIKE FICO CLASSIC AND FICO 10T: VantageScore’s use of large data sets and alternative data inputs allows millions more consumers to obtain a credit score. Rental, telecom, utility payment history, trended credit data, and machine learning enable VantageScore 4.0 to score consumers who remain invisible to legacy scoring approaches despite demonstrating strong repayment potential.

VANTAGESCORE 4.0 LENDING OPPORTUNITIES EXTEND FAR BEYOND FIRST-TIME HOMEBUYERS: The largest newly scoreable population with VantageScore 4.0 is not young or credit-inexperienced. Roughly 24 million consumers have established credit histories that have simply become dormant, with 77% scoring Near Prime or Prime under VantageScore 4.0.

EXPANDING ACCESS WITH VANTAGESCORE 4.0 DOES NOT MEAN EXPANDING RISK: Statistical testing of VantageScore 4.0 found that newly scoreable consumers exhibit default behavior comparable to, or better than, traditionally scored borrowers at the same score levels, demonstrating that “a VantageScore 620 is a VantageScore 620” regardless of whether the borrower was previously visible to legacy models.

Download the study here.

VantageScore 4.0 offers lenders the opportunity to responsibly identify more qualified borrowers by using modern, data-driven, and predictive scoring. For more information on VantageScore’s credit scoring models or to pilot VantageScore 4.0, please visit www.vantagescore.com/lenders.

About VantageScore®

VantageScore is the fastest-growing credit scoring company in the U.S., and is known for the industry’s most innovative, predictive and inclusive credit score models. In 2024, usage of VantageScore increased by 55% to hit 42 billion credit scores. More than 3,700 institutions, including nine of the top 10 U.S. banks, use VantageScore credit scores and digital tools to provide consumer credit products or generate greater insights into consumer behavior. The VantageScore 4.0 credit scoring model scores 33 million more people than traditional models. With the FHFA allowing the immediate use of VantageScore 4.0 for Fannie Mae and Freddie Mac guaranteed mortgages, the company is also ushering in a new era for mortgage lending.

VantageScore is an independent joint venture company owned by Equifax, Experian and TransUnion.

| ____________________________ |

| 1 This study was completed by OGMA Risk & Analytics and funded by VantageScore. |

Contacts

Yani Pena | VantageScore

Email: yani@vantagescore.com

Phone: +1 (415) 740-1519