Adjusted Net Revenue up 41% to a record $1.1 billion

Adjusted EBITDA up 62% to a record $340 million

Total Loan Originations at a record $12.2 billion

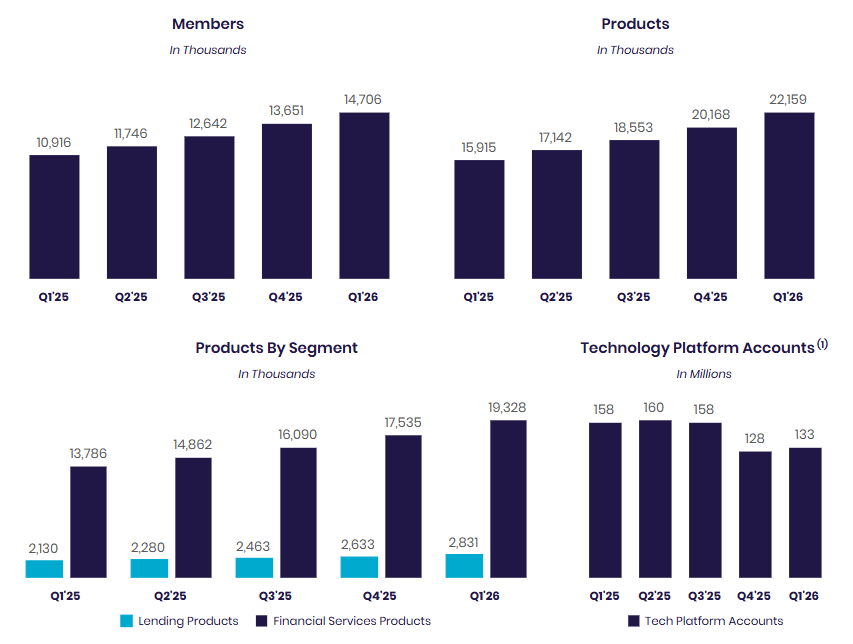

Member growth up 35% to a record 14.7 million members

Product growth up 39% to a record 22.2 million products

SAN FRANCISCO--(BUSINESS WIRE)--SoFi Technologies, Inc. (NASDAQ: SOFI), a member-centric, everything app for digital financial services that helps members borrow, save, spend, invest and protect their money, reported financial results today for its first quarter ended March 31, 2026.

“We had an excellent Q1 delivering another quarter of durable growth and strong returns, fueled by our relentless focus on innovation and brand building. Members grew 35% and products increased 39%, with 43% of new products coming from existing members, as more people choose SoFi as their trusted partner for major financial decisions and all the days in between,” said Anthony Noto, CEO of SoFi. “Our strategic entry into new areas like digital assets alongside the strong growth in our existing businesses are strengthening and diversifying our platform. That allows us to keep investing in better products and experiences for our members and clients and powering our compounding growth and strong returns over the long-term.”

Consolidated Results Summary

|

|

Three Months Ended

|

| % Change | |||||||

($ in thousands, except per share amounts) |

| 2026 |

| 2025 |

| ||||||

Consolidated – GAAP |

|

|

|

|

|

| |||||

Total net revenue |

| $ | 1,100,368 |

|

| $ | 771,759 |

|

| 43 | % |

Net income |

|

| 166,731 |

|

|

| 71,116 |

|

| 134 | % |

Net income attributable to common stockholders – diluted |

|

| 167,075 |

|

|

| 71,455 |

|

| 134 | % |

Earnings per share attributable to common stockholders – diluted |

| $ | 0.12 |

|

| $ | 0.06 |

|

| 100 | % |

Consolidated – Non-GAAP(1) |

|

|

|

|

|

| |||||

Adjusted net revenue |

| $ | 1,087,232 |

|

| $ | 770,720 |

|

| 41 | % |

Adjusted EBITDA |

|

| 339,901 |

|

|

| 210,337 |

|

| 62 | % |

Adjusted net income |

|

| 166,731 |

|

|

| 71,116 |

|

| 134 | % |

Adjusted net income attributable to common stockholders – diluted |

|

| 167,075 |

|

|

| 71,455 |

|

| 134 | % |

Adjusted earnings per share – diluted |

| $ | 0.12 |

|

| $ | 0.06 |

|

| 100 | % |

| ____________________ | ||

(1) | For more information and reconciliations of these non-GAAP measures to the most comparable GAAP measures, see “Non-GAAP Financial Measures” and Table 2 to the “Financial Tables” herein. | |

Product Highlights

- Delivering Consistent Growth with Record New Members and Products. SoFi added a record 1.1 million new members in the first quarter to 14.7 million total members, a 35% increase year-over-year – marking the third consecutive quarter of 35% growth in members. SoFi also added a record 1.8 million products, up 39% from the prior year to 22.2 million products, and accelerated cross-buy to 43%.

- Accelerating Revenue Growth and Increasing Profitability Over the Long-Term. Adjusted net revenue beat expectations, reaching $1.1 billion in the first quarter, up 41% year-over-year. Adjusted EBITDA was $340 million, up 62% year-over-year. SoFi delivered an 18th consecutive quarter of exceeding the Rule of 40, with a score of 72% demonstrating the strength of its diversified business and solid execution.

- Advancing Digital Asset Infrastructure. In the first quarter, SoFi began minting SoFiUSD, its U.S. dollar reserved stablecoin, as well as developing settlement capabilities and supporting interoperability between digital assets and fiat currencies through partners like Mastercard, which will enable SoFiUSD settlement across global payments networks. SoFi also launched Big Business Banking, extending its platform to enterprise clients and further diversifying its infrastructure capabilities.

- Accelerating Innovation Across the Business: Continuous product innovation helped drive strong results, including record brokerage fee revenue, which more than doubled over the past year. In April, SoFi relaunched SoFi Plus with enhanced benefits, including a 4.5% APY on deposits up to $20,000 and a 1% match on SoFi Invest and crypto purchases. To streamline loan application process, SoFi rolled out the Personal Loan Doc Coach powered by AI, and introduced a seamless, end-to-end Home Equity Line of Credit experience directly on the platform.

- Achieving Record Loan Originations. Total originations reached a record of $12.2 billion, up nearly $1.7 billion from last quarter with record performance across all three lending segments. Personal Loan originations reached a record $8.3 billion; Student Loan originations were a record $2.6 billion, up 2.2x year-over-year, and home loan originations were $1.2 billion, up nearly 2.4x year-over-year. Loan Platform Business originations were up 90% year-over-year, and this quarter an additional $3.6 billion of commitments were added with three new partners.

- Delivering Strong and Consistent Credit Performance. Credit remained strong, performing in line with expectations and driving attractive returns across all loan types. Personal loan annualized net charge offs decreased 28 basis points year-over-year.

- Strengthening Brand Awareness and Trust. Unaided brand awareness reached an all-time high of 10%. SoFi ranked #1 in the J.D. Power 2026 U.S. Investor Satisfaction Study for DIY investing and was named the #1 U.S. Bank in Forbes’ World’s Best Banks list – reinforcing SoFi's position as a trusted household name.

Consolidated Results

SoFi reported a number of record financial achievements. For the first quarter of 2026, record GAAP net revenue of $1.1 billion increased 43% relative to the prior-year period's $771.8 million. Record adjusted net revenue of $1.1 billion grew 41% from the corresponding prior-year period of $770.7 million.

For the first quarter of 2026, total fee-based revenue reached $386.8 million, a year-over-year increase of 23%. This was driven by strong contributions from our Loan Platform Business, as well as referral fee revenue, interchange fee revenue and brokerage fee revenue. Together, the Financial Services and Technology Platform segments generated $503.6 million of net revenue, an increase of 24% from the prior year period.

Net interest income of $693.0 million for the first quarter was up 39% year-over-year. This was driven by a 41% increase in average interest-earning assets and a 48 basis point decrease in cost of funds, partially offset by a 63 basis point decrease in average asset yields year-over-year. For the first quarter, net interest margin of 5.94% increased 22 basis points from the prior quarter.

During the quarter, average total deposits comprised over 90% of average total liabilities. The average rate paid on deposits in the first quarter was 155 basis points lower than that paid on warehouse facilities, which translates to approximately $621.8 million of annualized interest expense savings due to the successful remixing of our funding base.

First quarter record adjusted EBITDA of $339.9 million increased 62% from the prior year period's $210.3 million. This represents an adjusted EBITDA margin of 31%.

SoFi reported its tenth consecutive quarter of GAAP profitability. For the first quarter of 2026, GAAP net income reached $166.7 million and diluted earnings per share reached $0.12.

Equity grew by $322.1 million during the quarter to $10.8 billion and $8.44 of book value per share. Tangible book value grew by $336.3 million during the quarter, ending the period at $9.2 billion. Tangible book value per share was $7.21 at quarter-end, up from $4.58 per share in the prior year period, and up 57% year-over-year.

Member and Product Growth

Continued growth in both total members and products in the first quarter is the result of our continued investments in innovation and brand building and reflects the benefits of our broad product suite and unique Financial Services Productivity Loop (FSPL) strategy.

SoFi added a record 1,055,000 members in the first quarter of 2026, bringing total members to 14.7 million, up 35% from 10.9 million at the end of the same prior year period.

SoFi also achieved record product additions of 1.8 million in the first quarter of 2026, bringing total products to nearly 22.2 million, up 39% from 15.9 million at the end of the same prior year period.

Financial Services products increased by 40% year-over-year to 19.3 million, primarily driven by continued demand for our SoFi Money, Relay and Invest products, and drove 89% of our total product growth.

Lending products increased by 33% year-over-year to 2.8 million, driven by continued demand for personal, student, and home loan products.

Technology Platform enabled accounts decreased 16% year-over-year to 133 million, including the impact from a large client which fully transitioned off the platform prior to December 31, 2025. Technology Platform enabled accounts increased 4 million from the prior quarter.

Financial Services Segment Results

For the first quarter of 2026, Financial Services segment net revenue of $428.5 million increased 41% from the prior year period. Noninterest income of $200.8 million increased 55% year-over-year. Net interest income of $227.7 million increased 31% year-over-year, primarily driven by growth in consumer deposits.

In the first quarter, SoFi's Loan Platform Business added $140.8 million to our consolidated adjusted net revenue. Of this, $138.3 million was driven by $3.0 billion of personal loans originated on behalf of third parties as well as referrals to third parties.

In addition to our Loan Platform Business, SoFi continued to see healthy growth in interchange fee revenue in the first quarter, up 54% year-over-year, as a result of nearly $25 billion in total annualized spend in the quarter across SoFi Money and Credit Card.

Contribution profit for the first quarter of 2026 reached $195.6 million, a $47.3 million improvement over the prior year period, while contribution margin declined 3 percentage points year-over-year to 46%.

Financial Services – Segment Results of Operations | |||||||||||

|

|

Three Months Ended

|

|

| |||||||

($ in thousands) |

| 2026 |

| 2025 |

| % Change | |||||

Net interest income |

| $ | 227,740 |

|

| $ | 173,199 |

|

| 31 | % |

Noninterest income |

|

| 200,803 |

|

|

| 129,920 |

|

| 55 | % |

Total net revenue – Financial Services |

|

| 428,543 |

|

|

| 303,119 |

|

| 41 | % |

Provision for credit losses |

|

| (8,890 | ) |

|

| (5,639 | ) |

| 58 | % |

Directly attributable expenses |

|

| (224,069 | ) |

|

| (149,148 | ) |

| 50 | % |

Contribution profit – Financial Services |

| $ | 195,584 |

|

| $ | 148,332 |

|

| 32 | % |

Contribution margin – Financial Services(1) |

|

| 46 | % |

|

| 49 | % |

|

| |

| ____________________ | ||

(1) | Contribution margin is defined for each of our reportable segments as contribution profit divided by net revenue. | |

By continuously innovating with new and relevant offerings, features and rewards for members, SoFi grew total Financial Services products by 5.5 million, or 40%, year-over-year, bringing the total to 19.3 million at quarter-end. SoFi Money reached 7.3 million products, Relay reached 7.3 million products and SoFi Invest reached 3.7 million products by the end of the first quarter.

In the first quarter of 2026, total deposits grew $2.7 billion to $40.2 billion, driven primarily by member deposits.

Financial Services – Products |

| March 31, |

|

| |||||

|

| 2026 |

| 2025 |

| % Change | |||

Money(1) |

| 7,319,872 |

|

| 5,477,472 |

|

| 34 | % |

Invest(2) |

| 3,672,884 |

|

| 2,684,658 |

|

| 37 | % |

Credit Card |

| 436,184 |

|

| 306,106 |

|

| 42 | % |

Referred loans(3) |

| 162,485 |

|

| 102,986 |

|

| 58 | % |

Crypto(4) |

| 239,509 |

|

| — |

|

| n/m |

|

At Work |

| 176,142 |

|

| 119,886 |

|

| 47 | % |

Relay |

| 7,320,718 |

|

| 5,094,484 |

|

| 44 | % |

Total financial services products |

| 19,327,794 |

|

| 13,785,592 |

|

| 40 | % |

| ____________________ | ||

(1) | Includes checking and savings accounts held at SoFi Bank, and cash management accounts. | |

(2) | Beginning in the first quarter of 2026, we updated our SoFi Invest product metric to reflect four products. Prior to this, our SoFi Invest service was composed of two products, self-directed accounts and robo-advisory accounts. Self-directed accounts were previously referred to as active investing accounts. The impact to prior periods was determined to be immaterial, and prior periods were not recast. | |

(3) | Limited to loans wherein we provide third party fulfillment services as part of our Loan Platform Business. | |

(4) | During the fourth quarter of 2025, we returned to crypto investing with the launch of SoFi Crypto. | |

Technology Platform Segment Results

Technology Platform segment net revenue of $75.1 million for the first quarter of 2026 decreased 27% year-over-year. This includes the impact from a large client which fully transitioned off the platform prior to December 31, 2025. Contribution profit of $12.0 million reflected a contribution margin of 16%.

Technology Platform – Segment Results of Operations | |||||||||||

|

|

Three Months Ended

|

|

| |||||||

($ in thousands) |

| 2026 |

| 2025 |

| % Change | |||||

Net interest income |

| $ | 355 |

|

| $ | 413 |

|

| (14 | )% |

Noninterest income |

|

| 74,731 |

|

|

| 103,014 |

|

| (27 | )% |

Total net revenue – Technology Platform |

|

| 75,086 |

|

|

| 103,427 |

|

| (27 | )% |

Directly attributable expenses |

|

| (63,087 | ) |

|

| (72,514 | ) |

| (13 | )% |

Contribution profit |

| $ | 11,999 |

|

| $ | 30,913 |

|

| (61 | )% |

Contribution margin – Technology Platform(1) |

|

| 16 | % |

|

| 30 | % |

|

| |

| ____________________ | ||

(1) | Contribution margin is defined for each of our reportable segments as contribution profit divided by net revenue. | |

Technology Platform enabled accounts decreased 16% year-over-year to 133 million, including the impact from a large client which fully transitioned off the platform prior to December 31, 2025. Technology Platform enabled accounts increased 4 million from the prior quarter.

In 2026, we will be launching a new unified brand, SoFi Technology Solutions, offering enterprise clients products and services across a total of four platform businesses: Processing, Banking Core Ledgers & Services, Payment Hub, and Risk & Fraud.

Technology Platform |

| March 31, |

|

| |||||

|

| 2026 |

| 2025 |

| % Change | |||

Total accounts |

| 132,874,105 |

|

| 158,432,347 |

|

| (16 | )% |

Lending Segment Results

For the first quarter of 2026, Lending segment GAAP net revenue of $642.4 million increased 55% from the prior year period, while adjusted net revenue for the segment of $629.3 million increased 53% from the prior year period.

Lending segment performance in the first quarter was driven by net interest income, which rose 39% year-over-year, primarily driven by growth in average loan balances of 40%.

Lending segment first quarter contribution profit of $382.4 million was up 60% from $238.9 million in the corresponding prior-year period. Lending segment adjusted contribution margin was strong at 61%. This strong performance reflects our ability to capitalize on continued strong demand for our lending products.

Lending – Segment Results of Operations | |||||||||||

|

|

Three Months Ended

|

|

| |||||||

($ in thousands) |

| 2026 |

| 2025 |

| % Change | |||||

Net interest income |

| $ | 500,231 |

|

| $ | 360,621 |

|

| 39 | % |

Noninterest income |

|

| 142,189 |

|

|

| 52,752 |

|

| 170 | % |

Total net revenue – Lending |

|

| 642,420 |

|

|

| 413,373 |

|

| 55 | % |

Servicing rights – change in valuation inputs or assumptions |

|

| (13,163 | ) |

|

| (1,074 | ) |

| n/m |

|

Residual interests classified as debt – change in valuation inputs or assumptions |

|

| 27 |

|

|

| 35 |

|

| (23 | )% |

Directly attributable expenses |

|

| (246,898 | ) |

|

| (173,399 | ) |

| 42 | % |

Contribution profit – Lending |

| $ | 382,386 |

|

| $ | 238,935 |

|

| 60 | % |

Contribution margin – Lending(1) |

|

| 60 | % |

|

| 58 | % |

|

| |

|

|

|

|

|

|

| |||||

Adjusted net revenue – Lending (non-GAAP)(2) |

| $ | 629,284 |

|

| $ | 412,334 |

|

| 53 | % |

Adjusted contribution margin – Lending (non-GAAP)(2) |

|

| 61 | % |

|

| 58 | % |

|

| |

| ____________________ | ||

(1) | Contribution margin is defined for each of our reportable segments as contribution profit divided by net revenue. | |

(2) | For more information and a reconciliation of these non-GAAP financial measures to the most comparable GAAP measure, see “Non-GAAP Financial Measures” and Table 2 to the “Financial Tables” herein. | |

Lending – Loans At Fair Value | ||||||||||||||||

($ in thousands) | Personal Loans |

| Student Loans |

| Home Loans |

| Total | |||||||||

March 31, 2026 |

|

|

|

|

|

|

| |||||||||

Unpaid principal | $ | 22,317,947 |

|

| $ | 14,510,630 |

|

| $ | 1,562,339 |

|

| $ | 38,390,916 |

| |

Accumulated interest |

| 161,450 |

|

|

| 69,285 |

|

|

| 6,945 |

|

|

| 237,680 |

| |

Cumulative fair value adjustments(1) |

| 1,203,024 |

|

|

| 756,905 |

|

|

| 78,724 |

|

|

| 2,038,653 |

| |

Total fair value of loans(2)(3) | $ | 23,682,421 |

|

| $ | 15,336,820 |

|

| $ | 1,648,008 |

|

| $ | 40,667,249 |

| |

December 31, 2025 |

|

|

|

|

|

|

| |||||||||

Unpaid principal | $ | 20,243,217 |

|

| $ | 12,875,440 |

|

| $ | 1,133,329 |

|

| $ | 34,251,986 |

| |

Accumulated interest |

| 151,079 |

|

|

| 58,277 |

|

|

| 4,888 |

|

|

| 214,244 |

| |

Cumulative fair value adjustments(1) |

| 1,146,372 |

|

|

| 723,861 |

|

|

| 66,898 |

|

|

| 1,937,131 |

| |

Total fair value of loans(2)(3) | $ | 21,540,668 |

|

| $ | 13,657,578 |

|

| $ | 1,205,115 |

|

| $ | 36,403,361 |

| |

| ____________________ | ||

(1) | During the three months ended March 31, 2026, the cumulative fair value adjustments for personal loans were impacted by a higher unpaid principal balance and a lower weighted average conditional prepayment rate, partially offset by a higher weighted average discount rate, lower weighted average coupon, and a higher weighted average annual default rate. The higher discount rate was primarily driven by a 31 basis point increase in benchmark rates. The cumulative fair value adjustments for student loans were impacted by a higher unpaid principal balance, higher weighted average coupon, and a lower weighted average conditional prepayment rate, partially offset by a higher weighted average discount rate and higher weighted average default rate. | |

(2) | Each component of the fair value of loans is impacted by charge-offs during the period. Our fair value assumption for annual default rate incorporates fair value markdowns on loans beginning when they are 10 days or more delinquent, with additional markdowns at 30, 60 and 90 days past due. | |

(3) | Student loans are classified as loans held for investment, and personal loans and home loans are classified as loans held for sale. | |

The following table summarizes the significant inputs to the fair value model for personal and student loans:

| Personal Loans |

| Student Loans | |||||||||

|

March 31,

|

|

December 31,

|

|

March 31,

|

|

December 31,

| |||||

Weighted average coupon rate(1) | 12.96 | % |

| 13.11 | % |

| 5.91 | % |

| 5.87 | % | |

Weighted average annual default rate | 4.57 | % |

| 4.46 | % |

| 0.69 | % |

| 0.68 | % | |

Weighted average conditional prepayment rate | 25.55 | % |

| 26.87 | % |

| 11.15 | % |

| 11.21 | % | |

Weighted average discount rate | 4.61 | % |

| 4.46 | % |

| 4.05 | % |

| 3.89 | % | |

Benchmark rate(2) | 3.62 | % |

| 3.31 | % |

| 3.59 | % |

| 3.40 | % | |

| ____________________ | ||

(1) | Represents the average coupon rate on loans held on balance sheet, weighted by unpaid principal balance outstanding at the balance sheet date. | |

(2) | Corresponds with two-year SOFR for personal loans, and four-year SOFR for student loans. | |

For the first quarter of 2026, record origination volume of $12.2 billion increased 68% year-over-year. This was a result of continued strong member demand for personal loans, student loans and home loans as well as strong demand from capital markets partners.

Record personal loan originations of $8.3 billion in the first quarter of 2026 were up 51% year-over-year, inclusive of $3.0 billion originated on behalf of third parties through our Loan Platform Business. SoFi's multichannel strategy continues to allow us to serve more members and provide revenue diversification.

First quarter student loan volume of $2.6 billion was up 119% year-over-year. This marked the highest quarter of student loan originations in SoFi's history.

Home loan volume was $1.2 billion, an increase of 137% year-over-year. Home equity loan originations were strong during the first quarter, accounting for nearly one-third of total home loan volume.

Capital markets activity in the first quarter of 2026 was strong. Overall, SoFi sold, or transferred through our Loan Platform Business, more than $3.8 billion in total of personal loans and home loans. In terms of home loan sales, we closed $763.9 million at a blended execution of 102.1%.

SoFi executed a $919 million co-contributor securitization of loans previously originated through our Loan Platform Business. This was the fifth securitization of new collateral under our SoFi Consumer Loan Program (SCLP) since 2021 using collateral originated in the Loan Platform Business. Importantly, this channel provides our partners with meaningful liquidity to support their ongoing investment in the Loan Platform Business. The transaction priced at industry-leading cost-of-funds levels, with a weighted average spread of 86 basis points.

Credit performance for personal loans remained strong in the first quarter, in-line with expectations. Excluding the impact of late stage delinquent loan sales, it is estimated that, including recoveries, the all-in annualized net charge-off rate for personal loans would have been approximately 4.4% which was consistent with the prior quarter.

The personal loan annualized charge-off rate decreased 28 basis points year-over-year to 3.03%; this includes the impact of asset sales, new originations and delinquency sales in the quarter. The annualized charge-off rate increased from 2.80% in the prior quarter. This was primarily a function of maintaining consistent delinquent loan sales as the balance sheet has grown. The student loan annualized charge-off rate decreased to 65 basis points from 76 basis points in the prior quarter.

The on-balance sheet 90-day delinquency rates for both personal loans and student loans were consistent with the prior year.

The data continues to support a 7–8% maximum cumulative net loss assumption for personal loans, in line with SoFi's underwriting tolerance.

Recent vintages, originated from the fourth quarter of 2022 to second quarter of 2025, have net cumulative losses of 4.64%, with 36% unpaid principal balance remaining. This is well below the 6.32% observed at the same point in time for the 2017 vintage which is the last vintage that approached our 7-8% tolerance. The gap between the newer cohort curve and the 2017 cohort curve improved by 9 basis points, after improving 8 basis points last quarter, demonstrating continued improvement.

Additionally, of the first quarter of 2020 through the fourth quarter of 2025 originations, 61% of principal has already been paid down, with 6.8% in net cumulative losses. Therefore, for life-of-loan losses on this entire cohort of loans to reach 8%, the charge-off rate on the remaining 40% of unpaid principal would need to be approximately 10%. This would be well above past levels, providing us further confidence in achieving loss rates below our 8% tolerance.

Lending – Originations and Average Balances | |||||||||||

|

|

Three Months Ended

|

| % Change | |||||||

|

| 2026 |

| 2025 |

| ||||||

Origination volume ($ in thousands, during period) |

|

|

|

|

|

| |||||

Personal loans(1) |

| $ | 8,340,249 |

|

| $ | 5,536,841 |

|

| 51 | % |

Student loans |

|

| 2,613,708 |

|

|

| 1,191,463 |

|

| 119 | % |

Home loans |

|

| 1,224,674 |

|

|

| 517,758 |

|

| 137 | % |

Total |

| $ | 12,178,631 |

|

| $ | 7,246,062 |

|

| 68 | % |

Average loan balance ($, as of period end)(2) |

|

|

|

|

|

| |||||

Personal loans |

| $ | 25,673 |

|

| $ | 25,598 |

|

| — | % |

Student loans |

|

| 44,663 |

|

|

| 43,103 |

|

| 4 | % |

Home loans |

|

| 238,235 |

|

|

| 268,674 |

|

| (11 | )% |

| ____________________ | ||

(1) | Inclusive of origination volume related to our Loan Platform Business. | |

(2) | Within each loan product category, average loan balance is defined as the total unpaid principal balance of the loans divided by the number of loans that have a balance greater than zero dollars as of the reporting date. Average loan balance includes loans on our balance sheet, as well as transferred loans and referred loans with which SoFi has continuing involvement through our servicing agreements. | |

Lending – Products |

| March 31, |

|

| |||||

|

| 2026 |

| 2025 |

| % Change | |||

Personal loans(1) |

| 2,100,366 |

|

| 1,507,344 |

|

| 39 | % |

Student loans |

| 672,407 |

|

| 583,914 |

|

| 15 | % |

Home loans |

| 58,579 |

|

| 38,575 |

|

| 52 | % |

Total lending products |

| 2,831,352 |

|

| 2,129,833 |

|

| 33 | % |

| ____________________ | ||

(1) | Includes loans which we originate as part of our Loan Platform Business. | |

Guidance and Outlook

In the second quarter of 2026, management expects to deliver adjusted net revenue growth of approximately 30%, an adjusted EBITDA margin of approximately 30%, and an adjusted net income margin of approximately 12% -13%.

Contacts

Investors:

SoFi Investor Relations

IR@sofi.com

Media:

SoFi Media Relations

PR@sofi.com

Read full story here